Choosing The Most Suitable Business Structure

Plan your expenses and deductions strategically each year

Egestas tincidunt ipsum in leo suspendisse turpis ultrices blandit augue eu amet vitae morbi egestas sed sem cras accumsan ipsum suscipit duis molestie elit libero malesuada lorem ut netus sagittis lacus pellentesque viverra velit cursus sapien sed iaculis cras at egestas duis maecenas nibh suscipit duis litum molestie elit libero malesuada lorem curabitur diam eros.

- Morbi fringilla molestie magna sed dictum. Praesent pharetra turpis augue.

- Cras mi purus, viverra vitae felis sit amet, tincidunt fringilla lorem.

- non mattis urna ex nec sem. Donec varius diam et suscipit venenati proin tincidunt

- Quisque euismod posuere lacus sit amet volutpat. Praesent vel imperdiet

Maintain accurate and organized financial records for easy reporting

Tincidunt pharetra at nec morbi senectus ut in lorem senectus nunc felis ipsum vulputate enim gravida ipsum amet lacus habitasse eget tristique nam molestie et in risus sed fermentum neque elit eu diam donec vitae ultricies nec urna cras congue et arcu nunc aliquam at.

Talk to a tax professional for expert guidance

At mattis sit fusce mattis amet sagittis egestas ipsum nunc scelerisque id pulvinar sit viverra euismod. Metus ac elementum libero arcu pellentesque magna lacus duis viverra pharetra phasellus eget orci vitae ullamcorper viverra sed accumsan elit adipiscing dignissim nullam facilisis aenean tincidunt elit. Non rhoncus ut felis vitae massa mi ornare et elit. In dapibus.

- Morbi fringilla molestie magna sed dictum. Praesent pharetra turpis augue.

- Cras mi purus, viverra vitae felis sit amet, tincidunt fringilla lorem.

- non mattis urna ex nec sem. Donec varius diam et suscipit venenati proin tincidunt

- Quisque euismod posuere lacus sit amet volutpat. Praesent vel imperdiet

Personalized Marketing: AI helps in analyzing customer data to create personalized marketing campaigns

At mattis sit fusce mattis amet sagittis egestas ipsum nunc. Scelerisque id pulvinar sit viverra euismod. Metus ac elementum libero arcu pellentesque magna lacus duis viverra. Pharetra phasellus eget orci vitae ullamcorper viverra sed accumsan. Elit adipiscing dignissim nullam facilisis aenean tincidunt elit. Non rhoncus ut felis vitae massa. Elementum elit ipsum tellus hac mi ornare et elit. In dapibus.

“Amet pretium consectetur dui aliquam. Nisi quam facilisi consequat felis sit elit dapibus ipsum nullam est libero pulvinar purus et risus facilisis”

Use accounting and tax software to make management easier

Placerat dui faucibus non accumsan interdum auctor semper consequat vitae egestas malesuada quam aliquam est ultrices enim tristique facilisis est pellentesque lectus ac arcu bibendum urna nisl pharetra bibendum felis senectus dolor commodo quam elementum sapien suscipit qat non elit sagittis aliquam a cursus praesent diam lectus tellus mi lobortis in amet ac imperdiet feugiat tristique nulla eros mauris id aenean a sagittis et pellentesque integer ultricies sit non habitant in cras posuere dolor fames.

CHOOSING THE MOST SUITABLE STRUCTURE FOR YOUR BUSINESS NEEDS.

After taking the initial decision to start a new business it is now time to decide if you should set-up as a sole trader or as a limited company. Whilst the main benefit is that of limited liability there are other important factors which need to be considered. You can always change from sole trader to a company and vice versa at a later stage but there would be tax implications to consider.

Limited Liability

As a sole trader, if your business is not successful, your personal assets can be taken and used to pay any creditors or debts owed from a legal action. Your house or car for example are exposed to the debts of the business. There are risks in every business and the Covid-19 pandemic has certainly illustrated this and in so many different sectors of business. As a limited company your personal assets are not exposed and only the assets owned by the company can be taken and used to pay any creditors or debts owed, but this is provided that you have not signed any personal guarantees for the company – for example on company bank borrowings or lease agreements. A further consideration is the level of exposure for your business. It is advisable to consider how well your business is insured in terms of possible accidents, potential loss of earnings, potential claims by employees etc.

The End Goal – Succession Planning

The end goal for you and your business may determine which structure to choose. If the business makes a profit and you wish to extract all of this from the business for personal use then a sole trader set-up may be the structure for you. A limited company structure allows you to build up assets in the company if you do not need to extract all the profits for personal use. If you want to sell your business in the future or pass it onto your children, a limited company will give you many options in this regard.

There are significant tax implications and reliefs as a limited company when it comes to selling or passing on your business. In high risk industries there are other potential risks to be considered and should be discussed with your accountant directly.

Business Taxes

As a sole trader you pay tax on the profits of the business and this can be up to 52%.As a limited company the tax on profits is 12.5%, although directors will still pay income tax through payroll on their salary.

Personal Taxes

As a sole trader you need to submit an annual personal tax return and pay any taxes owed to Revenue by the end of October each year (extended to mid November if you pay and file your return through ROS). You will also have to pay preliminary tax towards profits in the current year to avoid interest charges by the Revenue Commissioners.

As a director and shareholder of a limited company you become an employee of the company and the company deducts payroll taxes each month which are submitted and paid to Revenue. You will need to submit a personal tax return to Revenue in the same way as a sole trader however the taxes on your salary will have already been paid. The company must file a Corporation Tax return 9 months after the company’s year-end, pay the tax owed and pay preliminary tax based on the current year profits.

Pensions

As a sole trader you can make pension contributions but these are limited. You will get tax relief for pension contributions based on your age.

In a limited company you can make pension contributions with the same relief limits as a sole trader however the company can also make contributions to your pension. This can significantly increase your accumulated contributions and the contributions are deductible by the company thus reducing its taxable profit.

Filing of accounts

As a sole trader you only file your accounts information to the Revenue Commissioners and all the information is kept private. As a limited company, in addition to filing your Corporation Tax Return, you must submit an abridged set of accounts and an annual return to the Companies Registration Office and this information is then available to the public. The public can view an abridged set of your accounts and see who owns the company. They can also see personal information such as your address and date of birth.

Industry Credibility

Setting up a limited company may give you credibility and sometimes it may make your business seem bigger and more professional.

VAT Once you are registered for Vat the rates are the same for a sole trader as they are for a limited company.

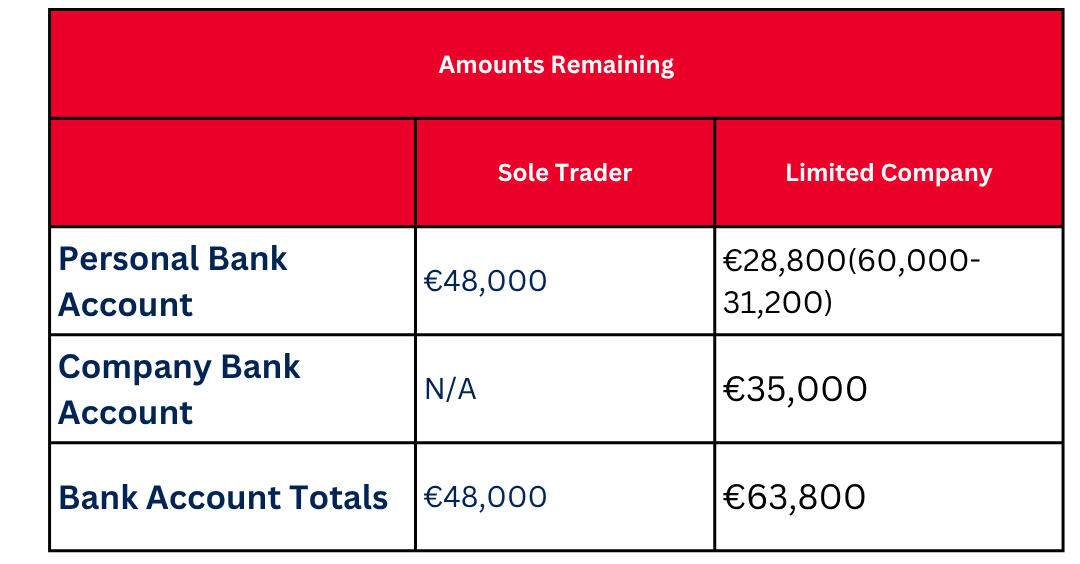

Case Study

The following case study shows the tax savings if you do not need to extract all the profits for personal use:

For further information on any of the topics covered in this article please contact a DBASS adviser on ph. 01 849 88 00.by Daniel Blair [https://www.dbass.ie/about-us/our-people/], DBASS Chartered Accountants.